I would read the second half of 2026 the way I would have from the allocator's seat: cautious, but selectively constructive.

The US–Iran ceasefire has pulled energy off its spring peak and lowered near-term recession risk, letting equities grind higher on resilient earnings. But the improvement is fragile: the Federal Reserve (“Fed”) seems to be leaning more hawkish; the labor market seems stable but could cool after summer, and the easing in geopolitical and energy risk may prove temporary. The October 2026 Fed meeting should be one to watch. If I were still running the portfolio, my posture would be to stay invested in quality and income while keeping selective hedges: favoring equities with valuation discipline and geopolitics-driven upside, higher-quality credit, and floating-rate income, while staying cautious on long duration, commercial real estate equity, and the most stretched AI-linked exposures.

Six Themes: Three Contrarian, Three Constructive

- Contrarian: In a note sent to Fortress clients earlier this year we highlighted the possibility that inflation is more likely to move higher than lower and, depending on several variables that we revisit below, could be north of 4% by year-end – higher than both the Federal Reserve estimates and the outer bound of the Bloomberg Contributor Composite.[1]

- Contrarian: In the same note, we demonstrated that if inflation does indeed move higher, the ten-year is likely mispriced and we would not be surprised to see a 5 handle on the 10-year by year end.

- Contrarian: We believe private credit could outperform median buyout private equity over the medium-term. Our reasons to prefer private credit in private markets are substantial and support a marginal dollar to private credit over private equity in asset allocation.

- We think it make sense to fade the duration rally that the consensus keeps waiting for until the inflation situation is clearer; consider staying in fixed income through TIPS. Nominal 10-year Treasuries near 4.5% may not compensate for the inflation path we expect. TIPS can deliver yield plus inflation protection.

- We are constructive but selective in credit – we believe bilaterally negotiated private credit presents better risk reward than public credit, which is typically covenant-lite and often long duration. Consider leaning into floating-rate and asset-based finance. Floating-rate middle-market credit at high single to low double digit all-in yield and asset-based finance, where collateral values inflate with the price level, or short duration allows reinvestment at higher rates, can be both defensive and offensive exposures in this environment.

- Own real assets. We think infrastructure with CPI-linked cash flows and gold are the cleanest expressions of the negative-real-rate trade. Gold’s structural support through central bank purchases should continue in the long term and it remains a historically valid geopolitical hedge, although a hawkish fed reduces gold demand in the near term.

Macro Framework

When we think about the second half of 2026, we start by thinking about what could impact clients and what we would be watching as allocators – (1) what are the known unknowns, (2) where is the 10-year and what is it telling us, and (3) based on 1&2 where is the macro environment highlighting risks and potential opportunities.

First, the known unknowns. We are watching:

- Energy & geopolitics. Oil and Middle East headlines into the midterms. A relapse toward $100 Brent could reopen the inflation and rate tail and pressure equities, while lifting energy and gold. We treat the current calm as relief, not resolution.

- The Fed versus a cooling labor market. Will slowing payrolls pull the Fed dovish or will sticky inflation force a hike? The outcome drives bonds, the cost of capital for private-credit borrowers, and rate-sensitive equities.

- AI-equity leadership versus credit stress. We see a widening gap between narrow, highly valued AI equity leadership and rising stress in AI/software-linked credit, with a heavier maturity wall arriving in 2028. A crack in either could ripple across equities (public and private) as well as private and structured credit.

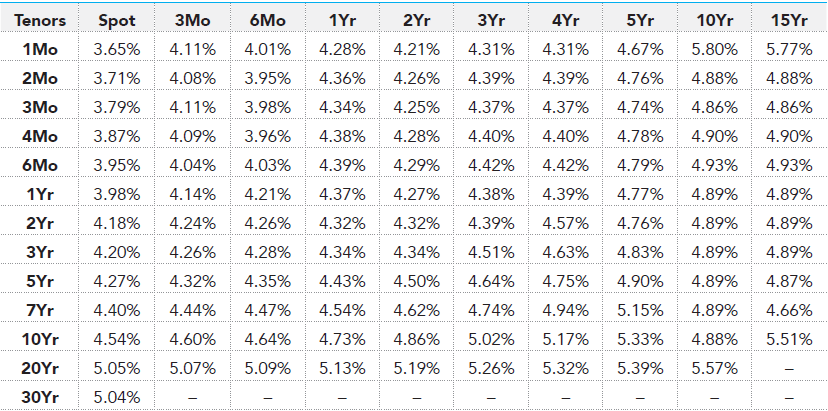

Second, the 10-year Treasury. As we enter the second half of the year with the 10-year near 4.5%, the message from the curve is that this cycle's rate regime is being repriced higher, not lower. With new leadership at the Fed signaling that further tightening may be needed and roughly half the FOMC now penciling in at least one hike before year-end, the front end is being pulled up by hike odds rather than the cuts the consensus spent last year waiting for. The result is an upward-sloping curve that reflects sticky inflation and a higher-for-longer policy path rather than a growth scare.

Another important signal sits in the forwards. The 5- and 10-year forward 10-year rates have climbed higher and remain elevated. The market is not simply repricing expected policy – it’s rebuilding term premium and marking up its estimate of neutral, driven by Treasury supply, the fiscal trajectory, and a less-credible disinflation path. In other words, the bond market increasingly treats higher long rates as structural rather than cyclical.

Figure 1: US Treasury Actives Forward Curve [2]

For positioning, our takeaway is twofold. First, the persistent post-COVID pattern of forecasters under-predicting yields argues for humility about calling a sustained rally in duration; the forwards are once again leaning higher than investors think. Second, the asymmetry cuts both ways - with this much term premium and hike risk already in the price, the sharpest move would come from a genuine growth crack, precisely the scenario in which today's elevated forwards would prove too high. I'd be patient on adding duration until that higher-for-longer thesis is meaningfully challenged.

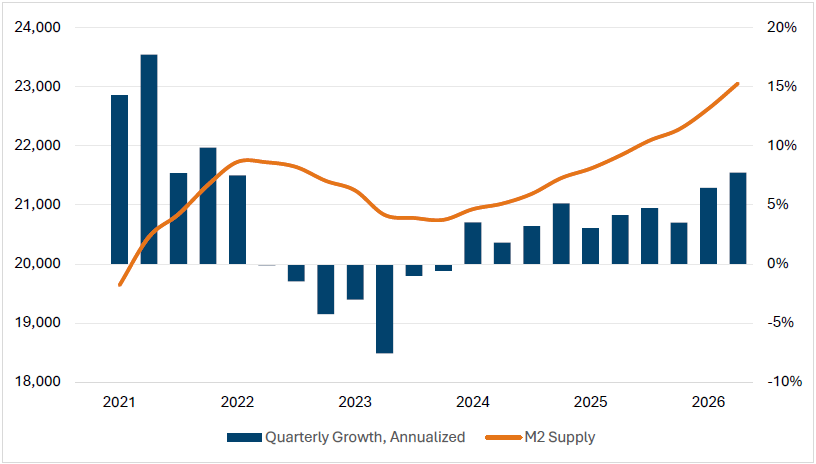

Third, the macro picture. Some conditions in place today are stimulative: M2 is reaccelerating at a nearly 7% quarterly annualized pace after contracting through 2022-2023. M2 velocity is recovering off its 2020 low; the Fed ended quantitative tightening in December 2025 and is buying $40 billion of T-bills a month under the label of “Reserve Management Purchases”; and real policy rates are barely positive against headline consumer price index (CPI) of 3.8% and core personal consumption expenditures (PCE) of 3.3%. Federal Reserve Chairman Warsh signaled in his first press conference as Chair that he could not categorize monetary policy as restrictive:

"And if I look at the housing markets as one example, Fed policy isn't the single determinant of the state of the housing market, but broadly I would say there Fed policy appears to be somewhat restrictive. I would have a hard time managing to say those words if I were to see what's happening in financial markets, so I'd say it's uneven." [3]

Figure 2: Money Supply ("M2") Growth [4]

That contradiction will likely resolve, potentially through a second inflationary wave in 2027 (in line with the historical average 12-to-18-month monetary lag from the M2 acceleration) at which point, depending on labor, the Fed will need to weigh tighten versus accepting structurally higher inflation. Neither outcome is benign for a standard 60/40 portfolio.

Given the uncertainty around the stability of the MOU between the US and Iran and the pace of reopening the Strait of Hormuz, and the challenge stagflation can present to a portfolio, I would prepare portfolios through the second half of 2026 for the wave, not the lull.

Footnotes

- 1. Bloomberg ECFC as of July 7, 2026. ↩

- 2. Bloomberg, June 24, 2026.↩

- 3. Kevin Warsh, Transcript of Chairman Warsh's Press Conference, Federal Reserve, June 17, 2026, page 6 of 21.↩

- 4. M2 (M2SL), FRED, St. Louis Fed, June 24, 2026.↩

Important Disclaimers

In general. This disclaimer applies to this document and the verbal or written comments of any person presenting it. This document, taken together with any such verbal or written comments, is referred to herein as the “Presentation.” Fortress Investment Group LLC, taken together with its affiliates, is referred to herein as “Fortress.” This Presentation is produced solely for the recipient and may not be transmitted, reproduced or made available to any other person.

No offer to purchase or sell securities. The Presentation does not constitute an offer to sell, or a solicitation of an offer to buy, any security and may not be relied upon in connection with the purchase or sale of any security. You are cautioned against using this information as the basis for making a decision to engage in any business relationship with Fortress or in connection with any transaction with Fortress.

Past performance. In all cases where historical performance is presented, please note that past performance is not a reliable indicator of future results and should not be relied upon for any reason.

No reliance, no update and use of information. You may not rely on the Presentation as the basis upon which to make any investment decision. To the extent that you rely on the Presentation in connection with any investment decision, you do so at your own risk. The Presentation does not purport to be complete on any topic addressed. Neither Fortress nor any of its representatives has made or makes any representation or warranty to any person regarding the Presentation. The information in the Presentation is provided to you as of the dates indicated and Fortress does not intend to update the information after its distribution, even in the event that the information becomes materially inaccurate. Certain information contained in the Presentation includes calculations or figures that have been prepared internally and have not been audited or verified by a third party. Use of different methods for preparing, calculating or presenting information may lead to different results and such differences may be material. Neither the issuance of this Presentation nor any part of its content is to be taken as any form of commitment on the part of Fortress to provide you with any additional information or to enter into any transaction or business relationship.

Forward looking statements. Forward looking statements (including estimated returns, opinions or expectations about any future event) contained in the Presentation are based on a variety of estimates and assumptions, including, among others, estimates of future operating results, the value of assets and market conditions at the time of disposition, and the timing and manner of disposition or other realization events. These estimates and assumptions are inherently uncertain and are subject to numerous business, industry, market, regulatory, geo-political, competitive and financial risks that are outside of the issuer’s control. There can be no assurance that any such estimates and assumptions will prove accurate, and actual results may differ materially, including the possibility that an investor may lose some or all of any invested capital. None of Fortress or any of their representatives has made or makes any representation to any person regarding any forward looking statements and none of them intends to update or otherwise revise such statements to reflect circumstances existing after the date when made or to reflect the occurrence of future events.

No tax, legal, accounting or investment advice. The Presentation is not intended to provide, and should not be relied upon for, tax, legal, accounting or investment advice. Any statements of federal tax consequences contained in the Presentation were not intended to be used and cannot be used to avoid penalties under the Internal Revenue Code or to promote, market or recommend to another party any tax related matters addressed herein.

Knowledge and experience. You acknowledge that you are knowledgeable and experienced with respect to the financial and business aspects of the Presentation and that you will conduct your own independent investigations with respect to the accuracy and completeness of the Presentation should you choose to use or rely on the Presentation, at your own risk, for any purpose.

Distribution of the presentation. Fortress expressly prohibits any redistribution of the Presentation without the prior written consent of Fortress. The Presentation is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use is contrary to law, rule or regulation.

Confidentiality. By accepting receipt or reading any portion of the Presentation, you agree that you will treat the Presentation confidentially. This reminder should not be read to limit, in any way, the terms of your (or your organization’s) confidentiality agreement with Fortress, if applicable. The information contained herein is confidential and proprietary in nature and may include information protected by relevant U.S. federal and state law governing the protection of trade secrets.